The Ins And Outs Of Home Mortgages

Content create by-Fink BorregaardBuying a home is a great time in anyone's life, but getting to that point for most people requires a home mortgage. This is where things can get complicated and delay the process of you actually purchasing your dream home. Don't wait until it is too late, get started now by reading the following article that shows what is needed to get approved for a home mortgage.

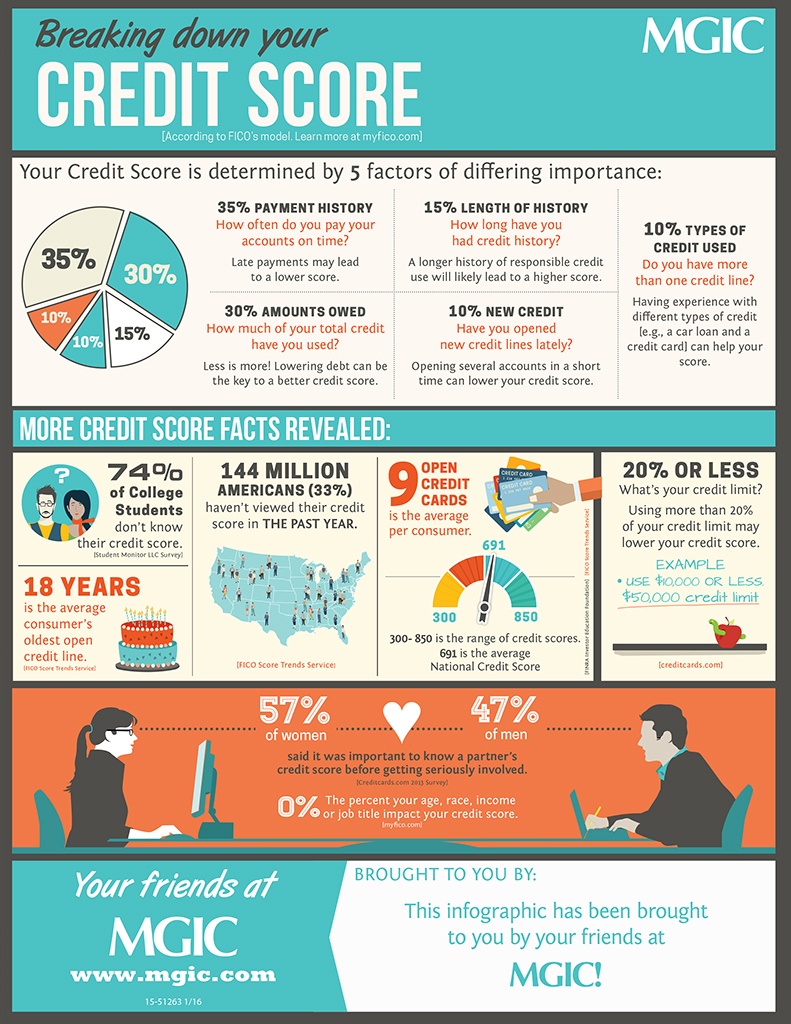

Remember that the interest rate isn't the most important part of a mortgage. You also have to think about closing costs, points and other incidentals. There are different kinds of loan as well. That is why you have to find out as much as you can about what you're eligible for.

Refinancing a home mortgage when interest rates are low can save you thousands of dollars on your mortgage. You may even be able to shorten the term of your loan from 30 years to 15 years and still have a monthly payment that is affordable. You can then pay your home off sooner.

Get pre-approved for a home mortgage before shopping for a new house. Nothing is worse than finding the perfect house, only to find out that you can't get approved for a mortgage. By getting pre-approved, you know exactly how much you can afford. Additionally, your offer will be more attractive to a seller.

You probably need a down payment. In years gone by, some lenders didn't ask for down payments, but those days are mostly over. You should ask how much you will have to spend on your down payment before submitting your application.

If one lender denies your mortgage loan, don't get discouraged. One lender's denial does not doom your prospects. please click the up coming document and investigate your options. Perhaps it will take a co-signer to help secure that loan for you.

When financing a house, giving a large down payment will result in a lower mortgage rate. This is due to the fact that a big down payment will reduce your loan to value ratio. When the loan to value ratio gets lower, the interest rates become more favorable for the home buyer.

Reducing https://saratogatodaynewspaper.com/today-in-saratoga/business/item/14779-community-bank-n-a-opens-business-banking-center as much as possible will increase your chances of being approved for a mortgage. If you are not in a good financial situation, meet with a debt consolidation professional to get out of debt as quickly as possible. You do not need to have a zero balance on your credit cards to get a mortgage but being deeply in debt is definitely a red flag.

Although using money given to you as a gift from relatives for your downpayment is legal, make sue to document that the money is a gift. The lending institution may require a written statement from the donor and documentation about when the deposit to your bank account was made. Have this documentation ready for your lender.

Take the time to get your credit into the best shape possible before you look into getting a home mortgage. The better the shape of your credit rating, the lower your interest rate will be. This will mean paying thousands less over the term of your mortgage contract, which will be worth the wait.

Use local lenders. If you are using a mortgage broker, it is common to get quotes from lenders who are out of state. Estimates given by brokers who are not local may not be aware of costs that local lenders know about because they are familiar with local laws. This can lead to incorrect estimates.

Whenever you go to apply for a mortgage it is best to have a good overall financial situation. You have to have some money set aside for closing costs, your down payment, and things like inspections, credit report fees, and everything else you're going to have to pay for. If you have a large down payment, you will have a better mortgage.

Learn about the three main types of home mortgage options. The three choices are a balloon mortgage, a fixed-rate mortgage, and an adjustable-rate mortgage (ARM). Each of these types of mortgages has different terms and you want to know this information before you make a decision about what is right for you.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

Many computers have built in programs that will calculate payments and interest for a loan. Use the program to determine how much total interest your mortgage rate will cost, and also compare the cost for loans with different terms. You may choose a shorter term loan when you realize how much interest you could save.

You may want to consider refinancing your home mortgage. Interest rates have gone down a great deal in recent years, and due to this you could pay thousands less over the term of your loan if you refinance now. This is something that you must consider if you are pay just a fraction of a percent more than what you could pay now.

Be prompt about getting your documentation to your lender once you have applied for a home mortgage. If your lender does not have all the necessary documentation on hand, and you have begun negotiations on a home, you could end up losing lots of money. Remember that there are nonrefundable deposits and fees involved, so you must get all your documentation submitted in a timely manner.

Get your credit under control. If you currently have a wallet full of plastic for every occasion, you should downsize. Having too much available credit can harm your loan, even if it is not debt. Close any non-essential accounts. Chose a gas card, a store card, and a single credit card to keep.

Now is the time to apply for that mortgage! The tips that you read should help guide you through this process. Now you just have to choose a lender and begin the process of applying for a loan.